Big, fake promises

"Get $50K–$250K even with bad credit!" If you've seen these ads, you've seen the problem. Those promises get people denied, or worse, stuck.

From a former banker, not a marketer

If you're tired of hearing a different answer from every bank, frustrated with getting underfunded, and confused by all the noise online, you're not alone. Most owners don't get denied because of their score. They get denied because of how they apply. I spent years inside the banking system approving and declining applications. Now I use that playbook to get owners like you the 0% cards, lines of credit, and term loans your profile actually supports.

Free 45-minute profile review. You pay nothing unless you're funded.

Why you're stuck

If you've been on Google, YouTube, or Instagram trying to figure this out, you've probably seen all three of these. They're why most owners stay stuck.

"Get $50K–$250K even with bad credit!" If you've seen these ads, you've seen the problem. Those promises get people denied, or worse, stuck.

Alternative lenders and merchant cash advances will get you money fast, then lock you into 30-60% effective rates and weekly debits that strangle the business you were trying to grow.

Good credit is not an approval strategy. Walk into a bank cold and you'll usually get underfunded, declined, or stuck with terms that don't fit. And every application leaves a mark on your credit report.

It's not your credit that's the problem. It's your approach.

The founder

I started my career inside a bank. I saw exactly how approval decisions get made, and how often deserving business owners were declined for reasons no one ever explained to them. I left because I didn't like how owners were treated.

Then I built my own company, ran it for 12 years, and sold it. Along the way I sat on your side of the desk too. I've been denied, I've felt the panic of not knowing where the next dollar of working capital was coming from. I know that fire.

Today I combine the banker's playbook, the operator's experience, and a financial advisor's discipline to do one thing: position your application so lenders see what your business is actually worth, and fund you on terms you can actually live with.

The Banker's Method

Two things almost nobody outside banking will tell you:

Beyond your FICO, every bank keeps an internal relationship score on you based on your history and behavior with them. Two owners with identical credit scores can walk out with completely different answers.

A $10,000 lump-sum deposit impresses no one. Steady $2K, $2K, $2K deposits month after month signal reliability. Reliability is what actually gets approved.

How we work

A real 45-minute call. We pull up your credit profile and your business together and I tell you straight what you actually qualify for. No charge, no obligation, no pitch.

I map exactly which products and which lenders fit your profile: 0% intro-APR cards for inventory, lines of credit for cash flow, term loans for bigger moves. Stacked the way a banker would design it.

We prepare and submit your applications the way an underwriter wants to see them. Strong profiles have been funded in as little as 30 days. You only pay our fee after the money hits your account.

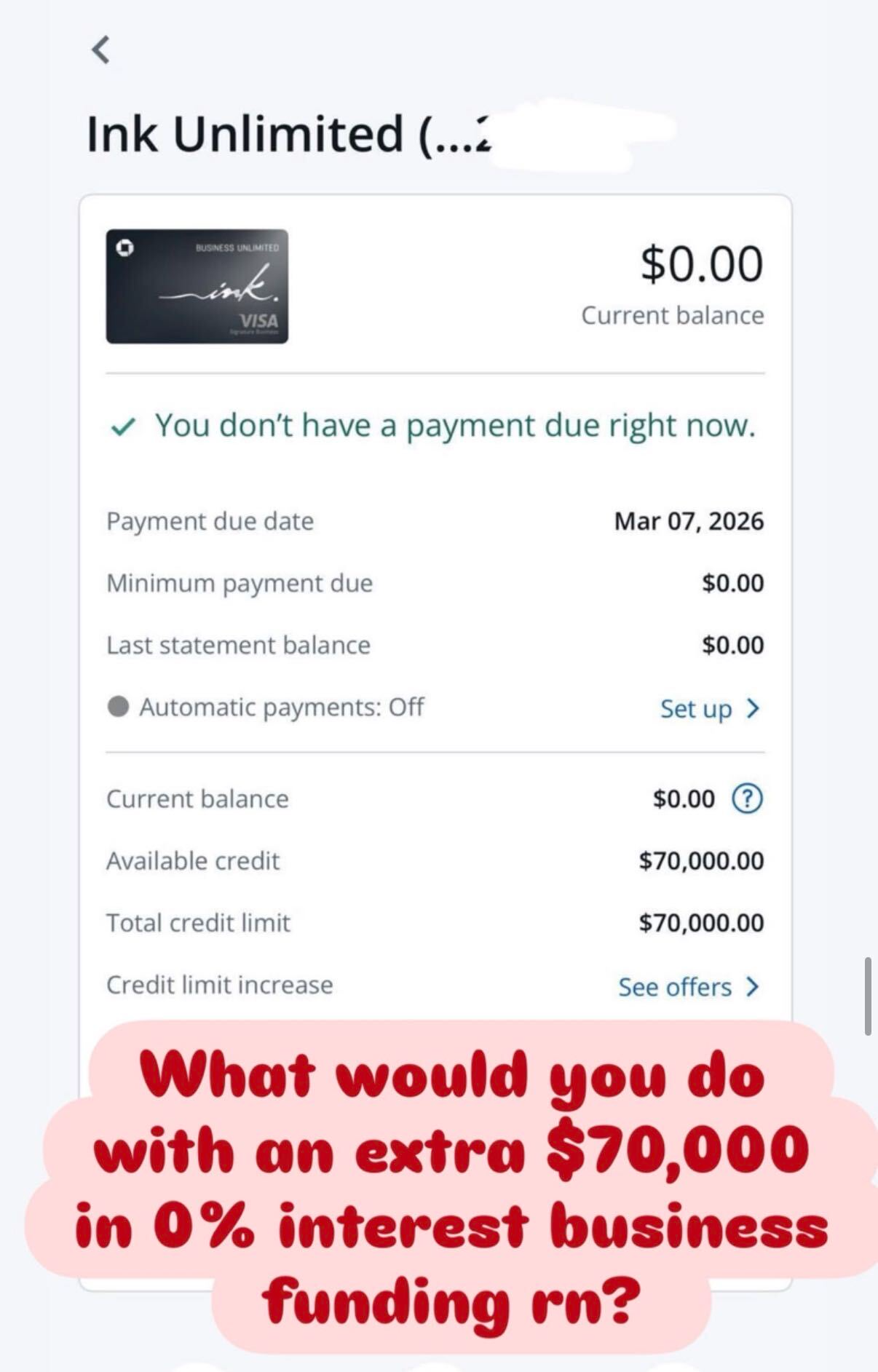

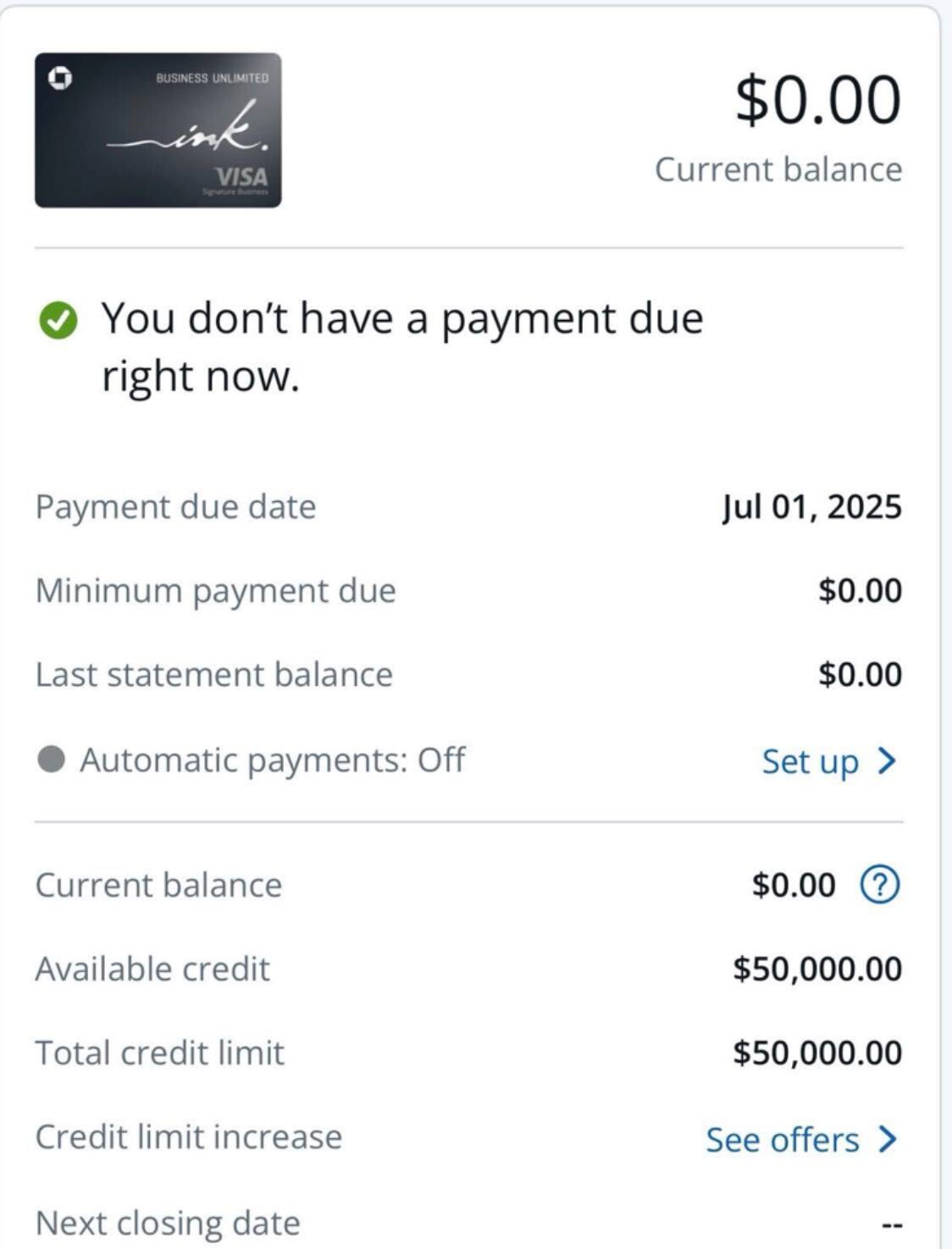

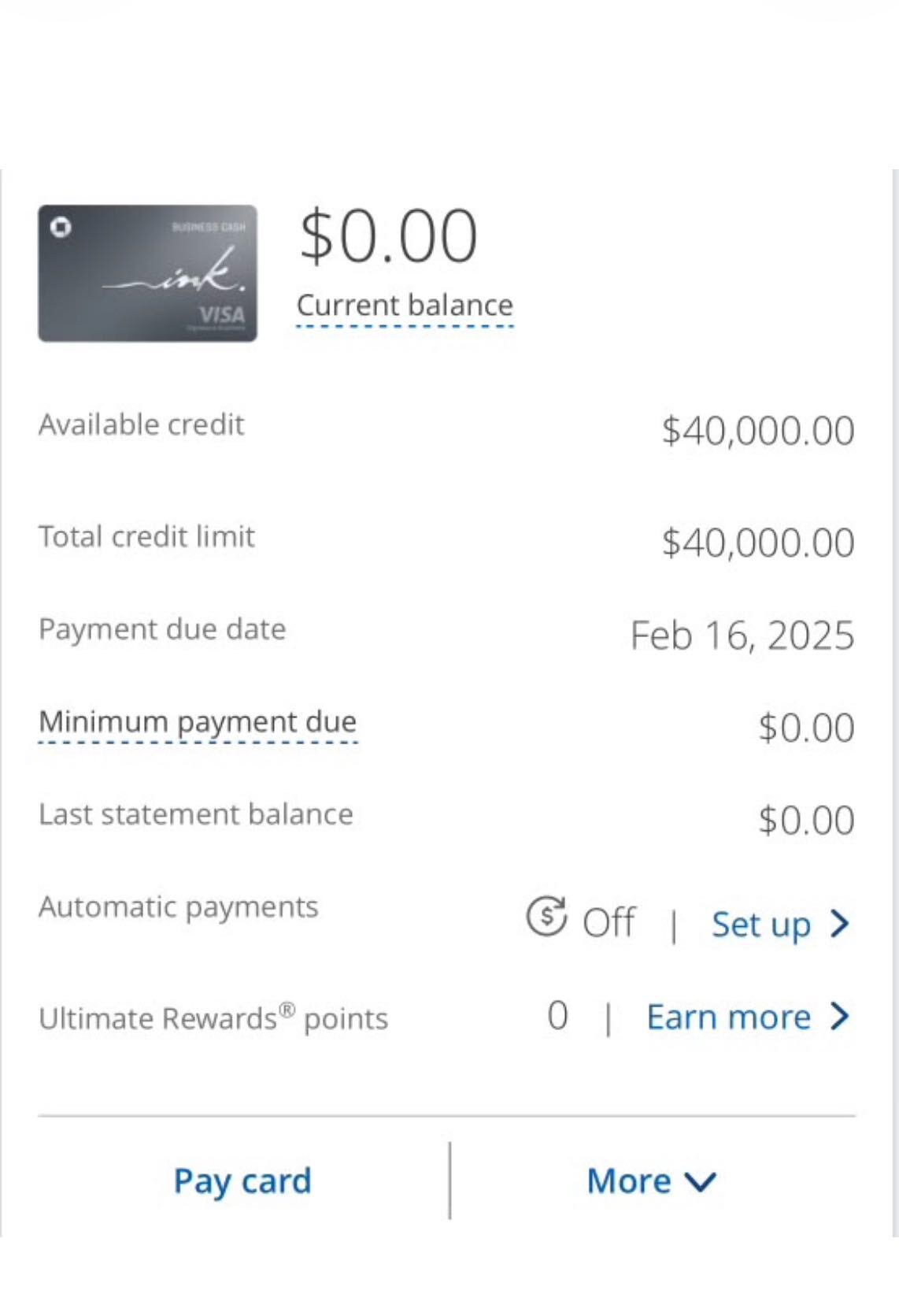

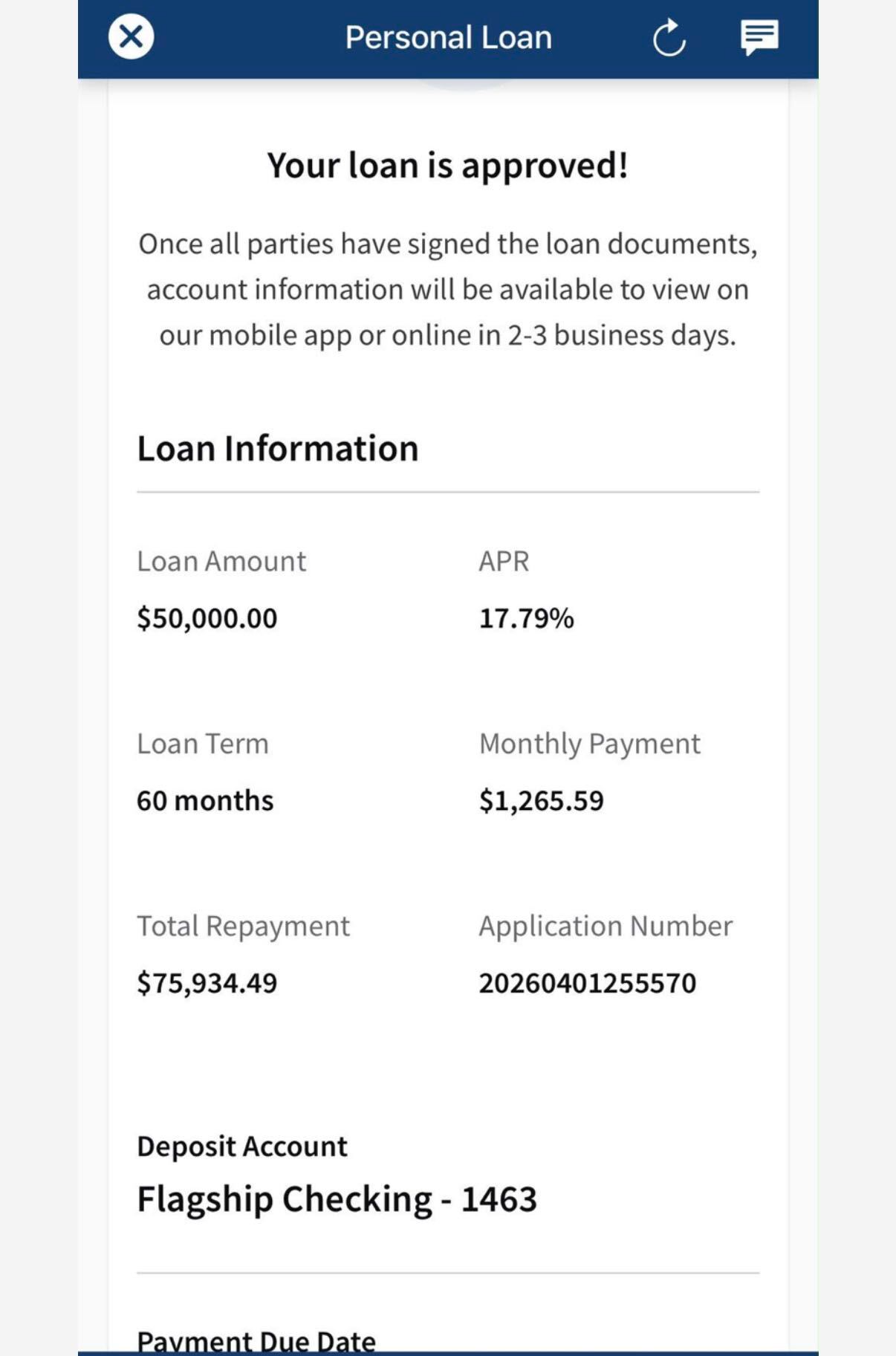

Receipts, not screenshots of stock photos

These are actual lender dashboards from clients we've worked with, shared with permission. Account numbers and names removed.

Individual results shared with client permission. Approval amounts, rates, and terms depend on your credit profile, business, and lender criteria. No specific outcome is guaranteed.

Honest outcomes

One client came to us paying over 100% effective interest between a private lender and merchant cash advances. We restructured his situation into a single term loan at 9%. Same business, same owner. A completely different future.

Individual results shared with client permission. Outcomes depend on your credit profile, business, and lender criteria. No specific amount or approval is guaranteed.

An interior design business owner with strong revenue and good credit had never leveraged financing. In about 30 days we secured a $50,000 line of credit, a $25,000 card, a second $25,000 line, and a $15,000 card. Over $100,000 in available capital, structured deliberately.

Individual results shared with client permission. Outcomes depend on your credit profile, business, and lender criteria. No specific amount or approval is guaranteed.

Fit check

Credit score below 680? Don't lie on the form to get past it. Tell us the truth and we'll route you to our credit improvement track, which is built to get you fundable as fast as possible.

Questions

Strong profiles have been funded in as little as 30 days. Timelines depend on your profile and the lenders we go to. We'll give you a realistic timeline on the call, not a fantasy.

It depends entirely on your profile. That's the honest answer. On the free call we'll tell you what your profile can realistically support. We don't quote dollar amounts before reviewing your situation, and you should be skeptical of anyone who does.

The review call is free. Our fee only applies after you actually receive funding. If you don't get funded, you don't pay us. We discuss the fee on the call once we know what your profile can do.

The review call involves no hard credit pull. Any applications are planned strategically with you, and we'll explain the credit impact of every step before we take it.

No. We don't sell courses, communities, or 'learn to do what we do' programs. This is a done-for-you service. You stay focused on running your business.

Then we'll tell you that honestly on the call. If you want, our credit improvement program can get you ready to qualify, usually in a matter of months, not years.

A free, honest 45-minute call with a former banker. No pressure, no fake promises. Just a straight look at your profile and your real options.